The Government of Canada, recognizing the importance of financial literacy, started Financial Literacy Month in 2010. Expanding on their efforts, the first National Financial Literacy Strategy (NFLS) was implemented in 2015 and was followed up by a second edition in 2021. As part of the NFLS and Financial Literacy Month, each November the federal government announces a theme for that year. This year’s theme is “Money on your Mind. Talk about it!”

For a long time talking about finances has been stigmatized. Subsequently, it’s a bit of a surprise that the government is encouraging more transparency. Why? What are the benefits?

Being more open about finances creates the opportunity to develop a financial support network. We can learn more about good money management practices and fundamental financial basics from each other. Financial transparency also curbs overspending. You feel more at ease to speak up when something doesn’t fit your budget or spending goals. Both of these things are key ingredients to financial well-being.

There’s one more element to this year’s theme. The government is asking Canadians to move past talk into action on just one thing. Whether it’s creating a budget, checking your credit report, or learning about compound interest, the goal is to complete one thing that improves our financial lives this November. In other words, they’re asking us to move the dial on our financial behaviours and attitudes.

Learning more

The Organisation for Economic Co-operation and Development (OECD) and the International Network on Financial Education (INFE) were wondering about the impact behaviours and attitudes have on a person’s financial life. To learn more they started conducting the International Survey of Adult Financial Literacy regularly since 2016. What they found is that a person’s financial well-being is heavily influenced by their financial attitudes and behaviours. While financial knowledge can be taught, a person’s financial attitudes and behaviours are mostly up to the discretion of the individual. In other words, it’s great to know something, but are you willing and able to put that knowledge to good use?

The findings of the 2023 survey revealed that there’s a lot of room for improvement. Only 51% of respondents met the minimum target behaviour score. Financial attitudes didn’t fair much better at an overall average of 56%.

What’s concerning is that these numbers have somewhat stagnated. In fact 2016 financial behaviour results were also 51%, Though financial attitude has seen some improvement from the 50% it was in 2016.

Canada only took part in the 2016 survey and faired reasonably well. Sixty-eight percent of Canadians met the minimum target behaviour score and 64% met the minimum target attitude score.

What are financial behaviours and attitudes?

For the purposes of the survey, financial attitude is characterized as whether a person has a preference for long-term financial security or short-term gratification. A person’s preference significantly influences how they manage their finances. Those who focus on long-term financial planning are characterized as having a high level of financial literacy.

Financial behaviours represent the actions individuals take regarding their finances, directly impacting their short- and long-term financial health. Some financially savvy behaviours the survey focused on were:

Keeping track of money flows: Regularly monitoring income and expenses, paying bills on time, and avoiding falling behind.

Saving and long-term planning: Developing a habit of saving money, avoiding borrowing for short-term needs, and setting long-term financial goals.

Making considered purchases: Seeking independent information and advice, comparing options from different providers, and shopping around for the best value before committing to a purchase.

These behaviours contribute to financial well-being by building financial resilience, enabling individuals to live within their means, and facilitating the achievement of long-term goals.

Changing behaviours and attitudes

Notice financial behaviours and attitudes in yourself you want to change? Here’s how.

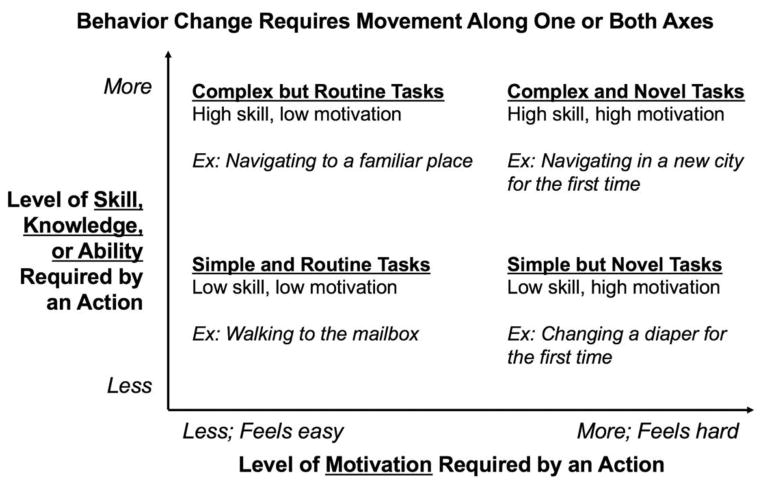

Elliot T Berkman a member of the Department of Psychology, Center for Translational Neuroscience, University of Oregon, and Berkman Consultants, LLC shared some insights in his article The Neuroscience of Goals and Behavior Change. He shares that successfully changing behaviour is based on two main factors, skill and motivation. Below is the chart they share showing how these two factors intersect in terms of behaviour changes.

For many of us financial literacy falls under the high skill, low motivation quadrant. Meaning many see it as hard to do and that there’s not much of a reward for doing it. This is why many of us continually place our finances on the back burner or never address them at all. Luckily he shares some insights, like The Habit Learning Process, on how to move a task along one or both axes to another quadrant. By improving your skillset or motivation the task gets easier, making it more likely to get done.

The Habit Learning Process

The Habit Learning Process uses a combination of pre-cues and rewards to help turn a hard task into a habit.

Pre-cue

The idea is to associate an environmental cue with the task. This way as soon as you see the cue your body and mind automatically start preparing themselves to do the task. He shares this example: “frequent association of a yellow light with a red light teaches experienced drivers to automatically move their foot to the brake when seeing a yellow light.”

Reward

It’s important not to choose just any reward. Choosing the right reward will give you the most reward bang for your buck. Berkman explains that some people are more inclined to get the most from extrinsic rewards while others prefer intrinsic rewards. The difference is that extrinsic rewards are more about achieving and intrinsic rewards are about mastering.

Bringing it all together

There are various places people get stuck when it comes to personal finances. Maybe you want to save more, pay off your debt or create a budget. If you’re struggling to make your goal happen you can use The Habit Learning Process to help.

Let’s use paying off debt as an example of how to utilize The Habit Learning Process with your finances. A common source of debt is impulse buying. Many people have found success by implementing a 24-hour waiting rule. When temptation strikes these people have a rule that they have to wait 24 hours before clicking buy. Often, their temptation wanes and they end up not buying the item. As a pre-cue, you could put a small sticky note on your credit card or computer reminding you of your 24-hour rule. When you follow through with waiting don’t forget to treat yourself to a reward suited perfectly to you.

Wrap up

The government and FCAC hit the nail on the head with this year’s “Money on your Mind. Talk about it!” Financial Literacy Month theme. There are many aspects of the theme that set people up to successfully boost their financial lives.

- Encouraging transparent financial discussions opens the opportunity to learn new skills and keep finances top of mind.

- Reducing overwhelm by asking people to simplify things by looking at just one aspect of finances.

Why are these approaches good for success? They mimic the proven behaviour change method The Habit Learning Process which combines pre-cues and rewards to establish effortless habits.

Decided your one thing for Financial Literacy Month is putting together a plan to get rid of your debt? The trained Credit Counsellor at Debt.ca can help. Contact us today for a free consultation.